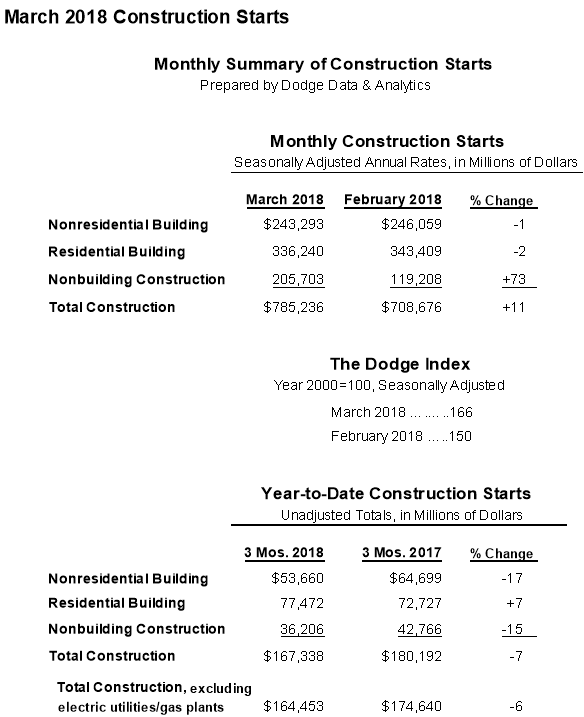

New construction starts in March increased 11 percent from the previous month to a seasonally adjusted annual rate of $785.2 billion, according to Dodge Data & Analytics. The substantial gain followed modest declines in January (down 2 percent) and February (down 3 percent), and brings the pace of total construction starts to the highest level over the past six months. The nonbuilding construction sector, comprised of public works and electric utilities/gas plants, soared 73 percent in March, boosted by the start of several very large projects.

New construction starts in March increased 11 percent from the previous month to a seasonally adjusted annual rate of $785.2 billion, according to Dodge Data & Analytics. The substantial gain followed modest declines in January (down 2 percent) and February (down 3 percent), and brings the pace of total construction starts to the highest level over the past six months. The nonbuilding construction sector, comprised of public works and electric utilities/gas plants, soared 73 percent in March, boosted by the start of several very large projects.

These included the $3.5 billion Mountain Valley Pipeline expansion in West Virginia and Virginia, the $1.1 billion I-405 highway project in Orange County, Calif., the $855 million Grand Parkway highway project in Houston, and a $400 million wind farm in Kansas. At the same time, both nonresidential building and residential building eased back slightly in March, with respective declines of 1 percent and 2 percent.

During the first three months of 2018, total construction starts on an unadjusted basis were $167.3 billion, down 7 percent from last year (which included exceptionally strong amounts for airport terminals and natural gas pipelines). On a 12-month moving total basis, total construction starts for the 12 months ending March 2018 were up 1 percent from the 12 months ending March 2017.

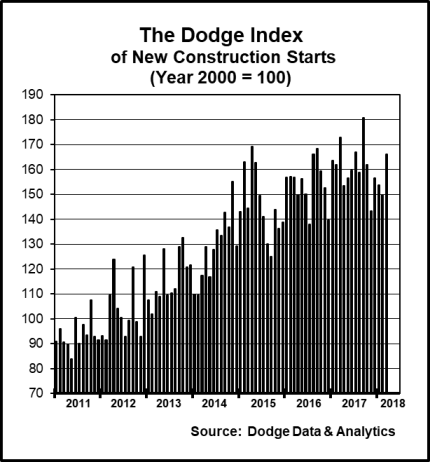

The March data produced a reading of 166 for the Dodge Index (2000=100), up from 150 for February. During the first quarter of 2018 the Dodge Index averaged 157, up 2 percent from the 154 average for last year’s fourth quarter, while slightly below the 161 average for the full year 2017.

“The construction start statistics can show wide swings month-to-month, and March certainly qualifies as one of the stronger months due to the inclusion of several very large projects,” stated Robert A. Murray, chief economist for Dodge Data & Analytics. “Looking at the data on a quarterly basis can reduce the volatility present in the monthly statistics, and this year’s first quarter shows a continuation of the up-and-down pattern that’s been present over the past year — first quarter 2017 up 10 percent, second quarter 2017 down 6 percent, third quarter 2017 up 8 percent, fourth quarter 2017 down 9 percent, and now first quarter 2018 up 2 percent.

This up-and-down pattern typically occurs when construction is at a mature stage of expansion, characterized by a slower rate of growth. A decelerating expansion does not necessarily mean that decline will closely follow, and there are several factors during 2018 that will help construction stay close to recent levels. In March, Congress reached agreement on fiscal 2018 federal appropriations, which provide additional funding for several public works programs, especially those that are transportation-related. Greater funding continues to be present from construction bond measures passed by state and local governments in recent years. The overall economy continues to proceed at a healthy clip, which supports healthy market fundamentals for commercial building. And, while interest rates are rising, the increases so far have been moderate, as shown by the ten-year Treasury bill stabilizing at 2.8 percent to 2.9 percent during March and the first half of April.”

Nonbuilding construction in March was $205.7 billion (annual rate), up 73 percent from the previous month. The substantial percentage gain was the result of very strong March (the third highest monthly amount over the past year) being compared to a weak February (the lowest monthly amount over the past year). The public works categories as a group climbed 62 percent in March, led by a 198 percent jump for the miscellaneous public works category which includes pipeline projects. The $3.5 billion Mountain Valley Pipeline expansion, which is a natural gas pipeline system that spans approximately 300 miles from northwestern West Virginia to southern Virginia, provided much of the lift in March. Highway and bridge construction climbed 29 percent in March, boosted by the start of such projects as the $1.1 billion I-405 highway project in Orange County CA, the $855 million Grand Parkway highway project in Houston, and the $318 million Kosciuszko Bridge replacement project (phase 2) in Brooklyn N.Y.

The river/harbor development category jumped 77 percent in March, aided by the start of a $580 million storm sewer and utility tunnel project in Washington DC and a $122 million harbor dredging project in Boston. Sewer construction in March was unchanged from February, while water supply construction fell 4 percent. The electric utility/gas plant category increased 507 percent in March, which was due to the comparison to an extremely low amount in February, as the March rate of construction starts was still 47 percent below its average monthly pace during 2017. Large electric utility/gas plant projects in March were a $400 million wind farm in Kansas, a $125 million liquefied natural gas plant in Texas, and two solar power facilities in Hawaii valued respectively at $125 million and $115 million.

Nonresidential building in March was $243.3 billion (annual rate), down 1 percent from the previous month. The commercial categories as a group retreated 13 percent following a 17 percent increase in February, with declines reported for four of the five structure types. Hotel construction dropped 40 percent after being boosted in February by the start of three large projects, including the $250 million Loew’s Kansas City Convention Hotel in Kansas City, Mo. In contrast, the largest hotel project entered as a March start was the $78 million Jimmy Buffett Margaritaville Hotel in Nashville, Tenn. Office construction in March dropped 16 percent after being lifted in February by the start of such projects as a $600 million Google data center in Clarksville, Tenn., and the $220 million Cerner Corporation Campus in Kansas City, Mo.

Still, March did include groundbreaking for several noteworthy office building projects, led by a $600 million Google data center in Pryor, Okla., the $245 million U.S. Citizenship and Immigration Services building in Suitland-Silver Hill, Md., the $233 million office portion of the $300 million One Willoughby Square mixed-used development in Brooklyn, NY, and the $137 million BMO Bank office tower in Milwaukee, Wisc. Store construction in March retreated 20 percent, while commercial garage construction slipped 7 percent. Warehouse construction was the one commercial structure type to report a March gain, rising 37 percent with the help of a $130 million Amazon fulfillment center in Rialto, Calif.

The institutional categories as a group fell 11 percent in March. Healthcare facilities retreated 32 percent following a 50 percent hike in February, although March did include the start of three hospital projects valued each at $100 million or more — the $344 million Indiana University Health Hospital and academic building in Bloomington, Ind., the $283 million Harrison Silverdale Hospital in Silverdale, Wash., and the $142 million Mercy Oklahoma Heart Hospital in Oklahoma City. Reduced activity in March was also reported for public buildings (courthouses and detention facilities), down 12 percent; amusement-related buildings, down 29 percent; and religious buildings, down 41 percent.

On the plus side, the educational facilities category increased 8 percent in March, led by two medical research facilities — the $200 million Children’s Mercy research tower in Kansas City and the $109 million Health Sciences Education Center in Minneapolis. March also saw the start of several large high school projects, including a $90 million high school in Indian Land, SC, and an $82 million high school expansion in Kirkland, Wash. Transportation terminal construction grew 40 percent from a weak February, helped by the start of a $154 million station improvement project on the Long Island Railroad in New York. Offsetting the overall declines for commercial and institutional building in March was a 280 percent jump by the manufacturing building category, which benefitted from the start of a $1.0 billion natural gas processing facility in Pierce CO, a $750 million chemical processing plant in Rosemount, Minn., a $500 million cryogenic natural gas processing plant in Slovan, Pa., and a $200 million cryogenic natural gas processing plant in Arkoma, Okla.

Residential building in March was $336.2 billion (annual rate), down 2 percent from the previous month. Multifamily housing slipped 7 percent following a 6 percent gain in February and a 36 percent hike in January. The number of large multifamily projects entered as construction starts stayed high, with March seeing 13 multifamily projects valued each at $100 million or more reach groundbreaking, slightly more than the 11 such projects entered as February starts (which included the $700 million City View Tower in Queens, NY).

The largest multifamily projects entered as construction starts in March were the $398 million multifamily portion of the $450 million Seattle Times mixed-use development in Seattle, the $220 million multifamily portion of the $250 million Broadway Block mixed-use development in San Diego and the $217 million multifamily portion of a $258 million mixed-use development in Weehawken, NJ. In March, the top five metropolitan areas ranked by the dollar amount of multifamily starts were — New York, Seattle, Boston, Los Angeles, and Miami. Metropolitan areas ranked 6 through 10 were — Washington D.C., Austin, San Diego, Denver, and Dallas-Ft. Worth. Single family housing in March was unchanged from February, extending the steady pace that was present during the previous four months.

The 7 percent decline for total construction starts on an unadjusted basis during this year’s January-March period compared to the last year reflected decreased activity for two of the three main sectors. Nonresidential building fell 17 percent year-to-date, with commercial building down 16 percent and institutional building down 24 percent, while manufacturing building grew 39 percent. Non-building construction fell 15 percent year-to-date, with public works down 10 percent and electric utilities/gas plants down 48 percent. Residential building grew 7 percent year-to-date, with single family housing up 4 percent and multifamily housing up 12 percent. By geography, total construction starts for the first three months of 2018 versus last year showed this performance — the South Atlantic, down 1 percent; the South Central, down 5 percent; the West, down 9 percent; the Midwest, down 10 percent; and the Northeast, down 14 percent.

Useful perspective comes from looking at 12-month moving totals, in this case the 12 months ending March 2018 versus the twelve months ending March 2017. On this basis, total construction starts were up 1 percent. By major sector, residential building advanced 3 percent, with single family housing up 7 percent while multifamily housing retreated 6 percent. Nonresidential building slipped 1 percent, with institutional building down 1 percent and commercial building down 6 percent, while manufacturing building climbed 32 percent. Nonbuilding construction was also down 1 percent, with public works up 2 percent and electric utilities/gas plants down 16 percent.