Corporates’ supply chain emissions are 26x higher than their operational emissions, finds report

September 9, 2024 — In 2023, corporates reported that their Scope 3 supply chain emissions were, on average, 26 times greater than their emissions from direct operations (Scopes 1 and 2). According to the new Scope 3 Upstream: Big Challenges, Simple Remedies report published recently by Boston Consulting Group (BCG) and CDP, upstream emissions from the manufacturing, retail and materials sectors had a footprint 1.4 times the total CO2 emitted in the EU in 2022.

However, supply chain emissions continue to be overlooked, with corporates twice as likely to measure operational emissions (Scopes 1 and 2) than their supply chain emissions (Scope 3). Furthermore, corporates are 2.4 times more likely to set targets for operational emissions compared with supply chain emissions. Of the corporates disclosing to CDP, only 15% have set a Scope 3 target.

These figures highlight that the challenge of effectively measuring Scope 3 emissions is widespread and spans industries. Meaningful strides toward emissions reductions require corporates to evaluate their full supply chain, then raise ambition and take accountability. The first step to driving meaningful change toward a 1.5°C-aligned net zero future begins with disclosure.

Sonya Bhonsle, director of strategic accounts at CDP

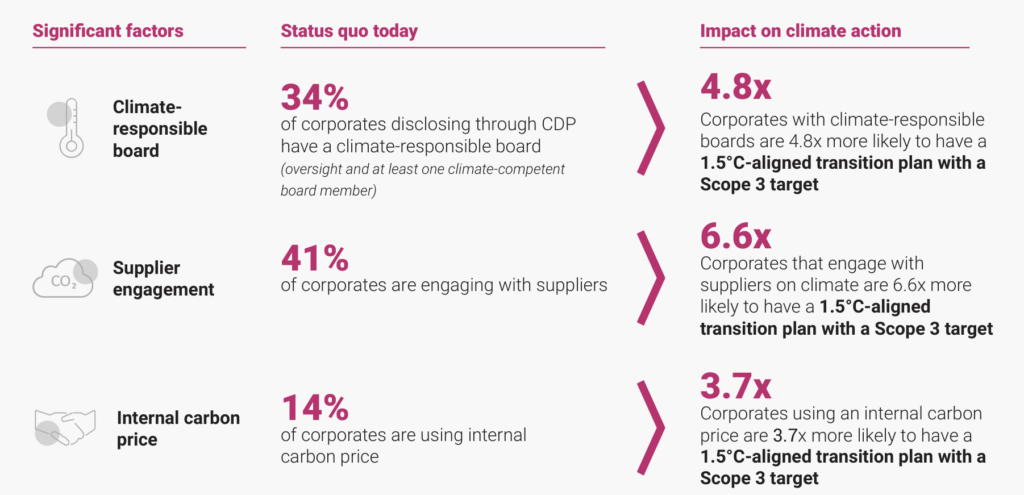

The report identifies the three most significant factors that correlate with ambition and action on Scope 3 upstream emissions:

- Climate-Responsible Board. Corporates with a climate-responsible board, which has climate oversight and competence, are 5x more likely to have a Scope 3 target and a 1.5oC-aligned transition plan

- Supplier Engagement Programs. Corporates that engage with suppliers on climate-related issues are almost 7x more likely to have a Scope 3 target and a 1.5oC-aligned transition plan. However, only four in ten corporates engage with their suppliers.

- Adoption of Internal Carbon Pricing. Corporates with an internal carbon price mandated for all business decisions are 4x more likely to have a Scope 3 target and a 1.5°C-aligned Scope 3 transition plan.

Disclosed upstream emissions from just the manufacturing, retail, and materials sectors in 2023 alone imply a carbon liability of over $335 billion. This liability is at risk of being overlooked by both corporates and investors.

The responsibilities and incentives to act on Scope 3 emissions for corporates and investors converge on risk management, and their oversight bodies must push for risk quantification and management.

Diana Dimitrova, BCG managing director and partner, and coauthor of the report

Only half of corporates disclosing through CDP evaluate the financial risks from upstream emissions; however, of those that do, a third acknowledge the risk to profit. Despite these risks, fewer than one in ten investors require investees to disclose Scope 3 upstream emissions as part of investment policies.

Boards have a fiduciary responsibility to manage these risks, and investors must price in the risks from carbon liability (business operational risk) and demand greater transparency through disclosure.

By prioritizing the three significant drivers, corporates can drive a step change in managing Scope 3 upstream emissions.

The Scope 3 Upstream: Big Challenges, Simple Remedies is available to download from CDP.