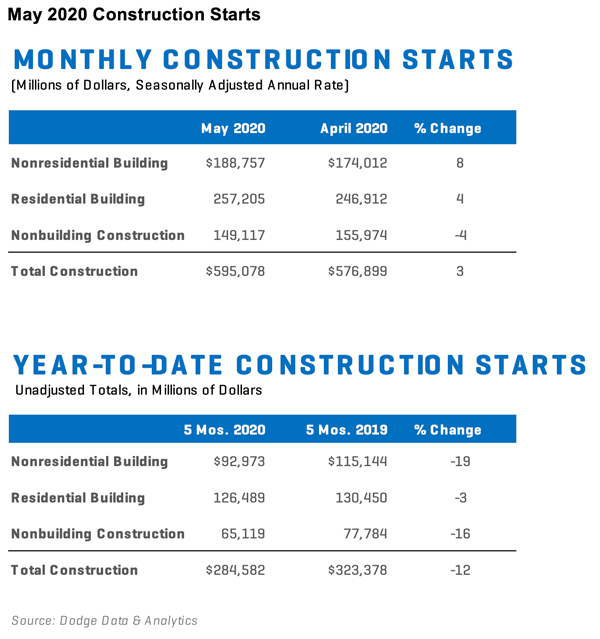

Total construction starts rose 3% from April to May to a seasonally adjusted annual rate of $595.1 billion, following a 25% decline the previous month. Several large nonresidential building projects broke ground in May resulting in the gain. Removing those large projects from the statistics would have resulted in no change in starts over the month. In May, nonresidential buildings increased 8%, while residential building starts rose 4%. Nonbuilding starts, however, declined 4% during the month.

Through the first five months of 2020, total construction starts were 12% lower than in the same period in 2019. Nonresidential starts were down 19%, nonbuilding starts were 16% lower, and residential starts were off 3%. For the 12 months ending May 2020, total construction starts were down 1% from the same period a year earlier. Residential buildings were 1% higher and nonbuilding starts were up 5%. Nonresidential starts, however, were 7% lower for the 12 months ending May 2020. The Dodge Index posted a slight gain, increasing to 126 (2000=100) in May from the 121 posted in April.

“While May’s increase in construction starts is certainly good news, the influence of several large projects undermines the notion that the construction sector has fully entered recovery,” stated Richard Branch Chief Economist for Dodge Data & Analytics. “Even as state and local areas re-open and bans on construction activity in Boston, New York City and other areas are lifted, the sector will have to contend with digging itself out from a deep economic recession. While the overall economy most likely hit bottom in May, the recovery will be slow since nearly 20 million jobs have been lost since February. The second half of 2020 will be a slog and gains will be modest over the short term.”

Nonbuilding construction fell 4% over the month in May to a seasonally adjusted annual rate of $149.1 billion. The utility/gas plant category dropped 37%, while the highway and bridge category lost 4%. On the plus side, the miscellaneous nonbuilding category increased 31% over the month and environmental public works were flat.

The largest nonbuilding project to break ground in May was the $1.3 billion widening of Interstate 635 in Dallas. Also starting in May were the $789 million Lynnwood Link Extension (Northgate to NE 200th) in Lynnwood, Washington, and the $705 million widening of I-405 in Seattle.

Year-to-date through May, nonbuilding construction starts were down 16% compared to the first five months of 2019. Starts in the highway and bridge category were up 5% through May, although other nonbuilding categories were down significantly. Environmental public works were down 24%, while the miscellaneous nonbuilding category was 31% lower. The utility and gas plant category was 35% lower through the first five months of this year. On a 12-month rolling basis, total nonbuilding starts were 5% higher than the 12 months ending May 2019. Starts in the utility/gas plant category were up 34%, while miscellaneous nonbuilding starts were 1% higher. Street and bridge starts were down 3% for the 12 months ending in May while environmental public works were 2% lower.

Nonresidential building starts rose 8% in May to a seasonally adjusted annual rate of $188.8 billion following the very steep April decline related to COVID-19. However, the rebound was due to several large projects that broke ground in the manufacturing, hotel, and education categories. Removing those projects would have led to a mild decline in nonresidential building starts in May. Commercial starts gained 6% in May and manufacturing starts rose 167%, but institutional building starts were flat.

The largest nonresidential building project to get underway in May was the $950 million SDI Steel Complex in Sinton, Texas. Also starting during the month was the $355 million Fig + Pico hotel towers in Los Angeles, and the $360 million Wolf Point South Tower B building in Chicago.

Through this year’s first five months, nonresidential building starts were 19% lower than in the first five months of 2019. Commercial starts were 24% lower, while institutional starts were down 11%, and manufacturing was off 39% through five months. Over the past 12 months, nonresidential building starts were down 7% from the prior 12 months. Commercial starts were 6% lower, while institutional starts were down 5% and manufacturing starts dropped 16%.

Residential building starts rose 4% in May to a seasonally adjusted annual rate of $257.2 billion. Single family starts rose 2%, while multifamily starts gained 10% over the month.

The largest multifamily structure to break ground in May was the $180 545 Vanderbilt Ave mixed-use development in Brooklyn, New York. Also starting was the $150 million 354 N Union apartment tower in Chicago IL and the $150 million Ripley II – Solaire 8200 Dixon Luxury Apartments in Silver Spring, Maryland.

Through the first five months of 2020 residential construction starts were down 3% versus the same time period in 2019. Single family starts were flat, while multifamily starts were down 12% through five months. For the 12 months ending in May, total residential starts were 1% higher than in the 12 months ending May 2019. Single family starts were up 3%, while multifamily building starts were down 2%.